White Label

Payment

Gateway

Launch and scale faster under your brand

Get more flexibility and enterprise‑grade security

Compliant by design. Controlled by you

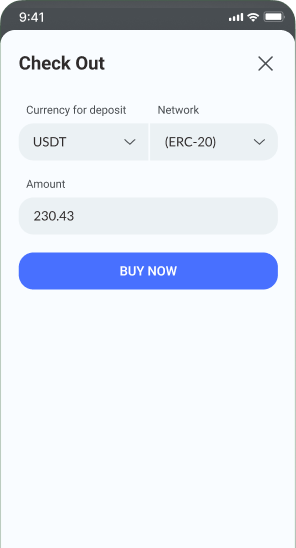

From seamless checkout to smart payments

Enable seamless payments across web and mobile

with a fully branded checkout experience and smart routing

Built for

Banks & Acquirers

Slow time-to-market, third-party dependency, limited control over checkout/brand.

- Fully branded gateway

- Control over checkout and flows

- Multi-merchant / multi-MID support with configurable hierarchy

- Tokenization + network token readiness for recurring payments

PSPs

Hard to differentiate and scale merchant onboarding with heavy ops and vendor lock-in.

- Custom checkout logic

- Rules-based routing and failover cascading to optimize approvals & cost

- Rapid new APMs/PSPs enablement without rebuilding checkout UX

- Configurable onboarding workflows

Payment Orchestrators

Need a stable gateway layer without building acceptance infrastructure from scratch.

- Ready-made gateway layer for orchestration stacks

- Connector framework to onboard providers faster

- Risk hooks: velocity rules + external fraud connectors

- High-availability support

Key Features

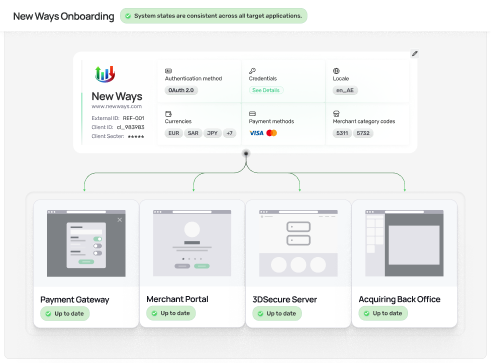

Merchant Onboarding

Customize onboarding and orchestrate frictionless and secure workflows to reduce cost and merchant registration time. Intuitive onboarding flow simplify gathering merchant information required for the application; Backend process management tool speeds up client’ scoring and due diligence routines

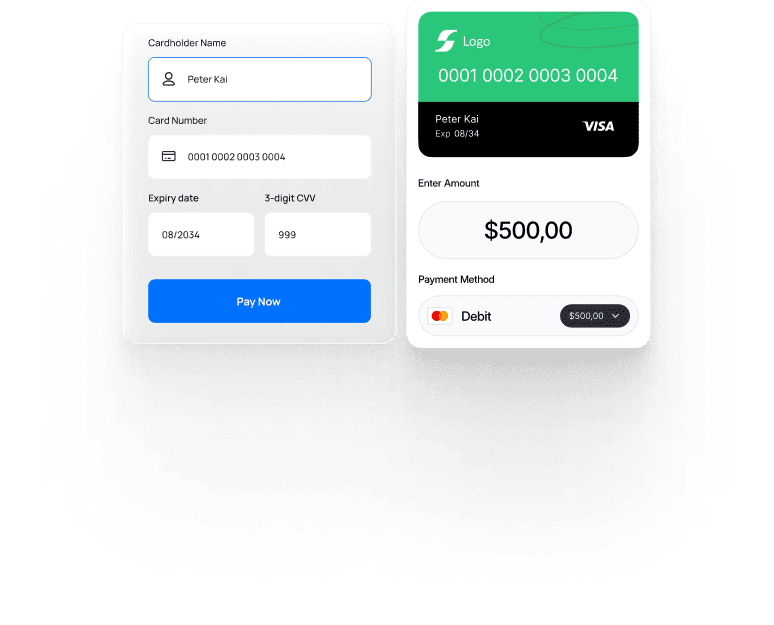

Smart Checkout

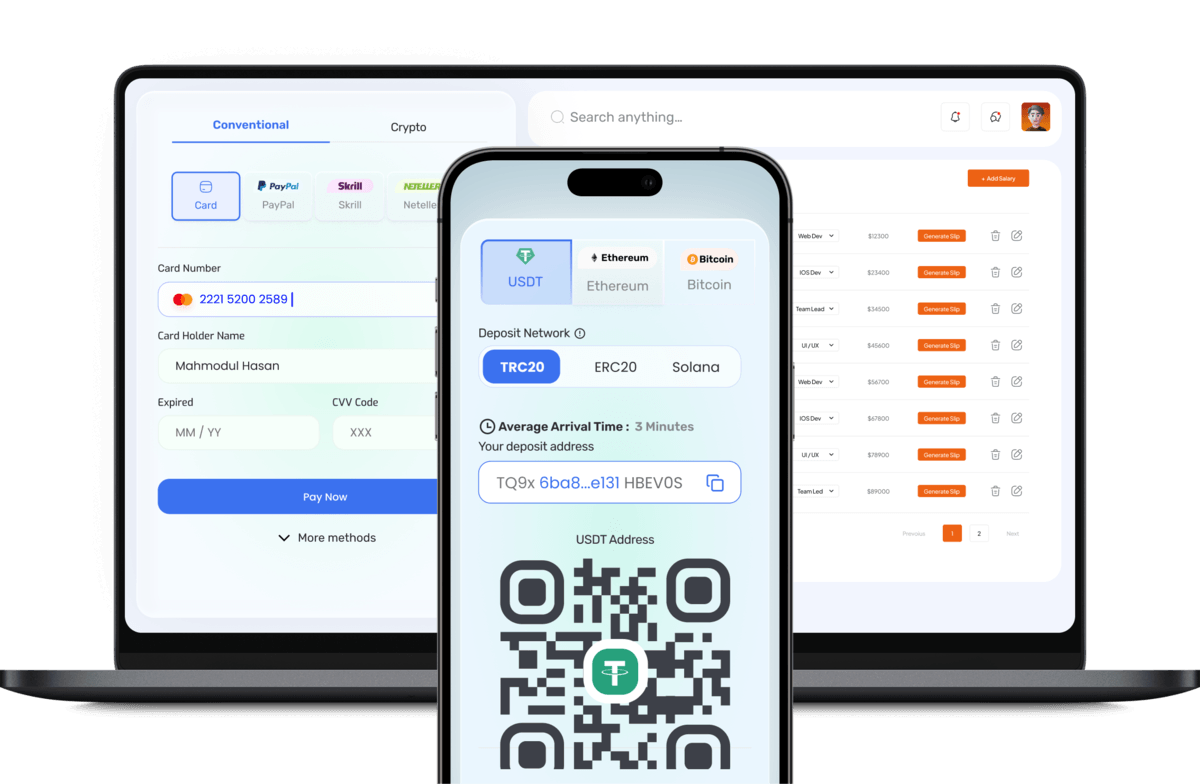

Hosted payment page can be seamlessly integrated into merchant websites and apps or loaded as a separate payment page. Create tailored payment pages with a personalized look, one-click check out or alternative payment methods

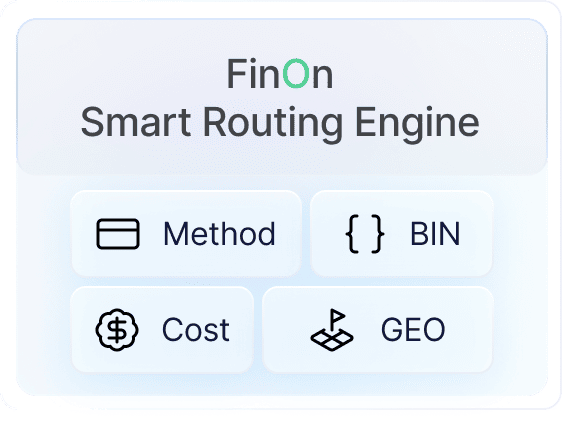

Intelligent transaction routing

Smart transaction routing engine enables high conversion rate by routing transactions to the best partner by Payment method, Currency, BIN country, Type of card, Amount, and many more

Merchant portal

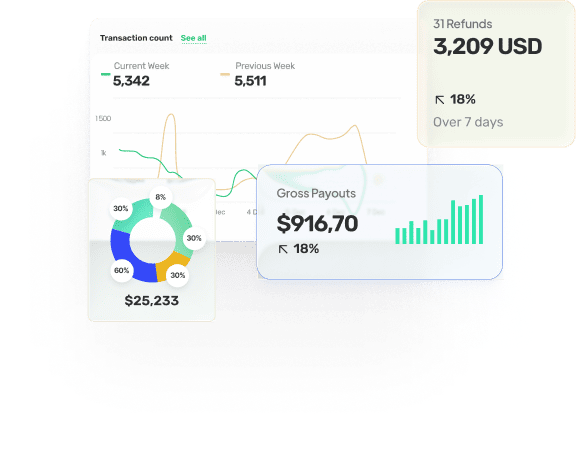

Merchants can manage all their payments from initiation to reversals and refunds via user-friendly merchant portal. Advanced reports and dashboards improve and accelerate decision making, provide more control and simplify reconciliation

EMV 3D SECURE

Payment Gateway fully supports 3DS 2.2 helping to prevent fraud and reduce friction allowing to authenticate high risk transactions with confidence, leading to a decrease in card declines and disputed transactions. Support 3DS SDK, a software for facilitating cardholder authentication that is embedded in a merchant mobile app

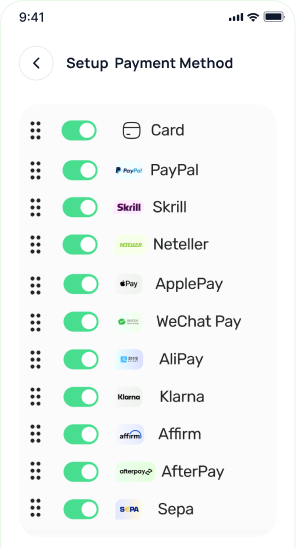

Alternative payment methods

Increase checkout conversions with alternative payment methods including Local Schemes, Open Banking, MOMO, Wallets, and BNPL providers. Multi-acquiring support gives PSPs exceptional flexibility and cost control over acquiring relationships

Risk management

Risk rules, smart limits along White/Black listing features in will protect from fraud and make smarter decisions. Support integration with external fraud and risk management systems

Billing and settlement

Gain the flexibility of tariff configuration, and pricing models, build payment schedules, manage your settlement cycles, and more with our platform

Integration types

Connect your branded gateway the way you want — fast, flexible, and fully under your control.

Mobile SDK

API rest/API soap

CMS plugins

Hosted payment page

See what your branded payment flow could look like

Frequently Asked Questions

A White-Label Payment Gateway is a fully branded

payment processing platform that allows banks, fintechs, acquirers, or PSPs to

offer payment services under their own brand, without building the

infrastructure from scratch.

It includes:

- Payment APIs

- Merchant portal

- Back-office

- Risk & fraud tools

- Settlement management

- Smart routing engine

All UI and API endpoints can be customized to reflect the client’s brand identity.

Smart Routing is an intelligent transaction

routing engine that dynamically selects the optimal acquirer, processor, or

payment channel for each transaction based on predefined rules and real-time

conditions.

Routing decisions can be based on:

- Card BIN

- Issuing country

- Card brand (Visa, Mastercard, etc.)

- Currency

- Merchant category (MCC)

- Transaction amount

- Authorization success rate

- Acquirer availability

- Cost optimization logic

The platform is suitable for:

- Banks launching acquiring services

- Fintech companies

- Payment Service Providers (PSPs)

- Payment Facilitators (PayFacs)

- Marketplaces and aggregators

- Cross-border e-commerce platforms

It allows them to operate as a full-scale payment gateway under their own brand.

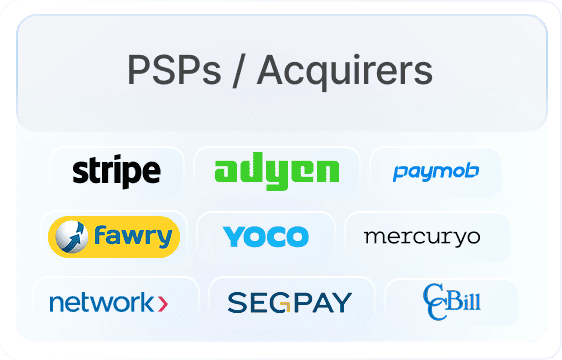

Yes. The platform supports multi-acquirer orchestration, enabling:

- Parallel acquirer connections

- Primary/secondary routing

- Geo-based routing

- Brand-based routing

- Cost-based optimization

- Failover routing

This increases authorization rates and reduces dependency on a single acquiring partner.

Smart Routing improves performance by:

- Routing domestic cards to domestic acquirers

- Sending high-risk transactions to specialized acquirers

- Avoiding overloaded or degraded endpoints

- Learning from historical approval patterns

- Automatic retry logic with alternative acquirers

This leads to measurable uplift in authorization success rates.

Yes. The routing engine can calculate:

- MDR differences between acquirers

- Interchange impact

- Scheme fees

- Cross-border fees

- FX margins

Transactions can be routed to minimize processing cost while maintaining approval rates.

The system supports both:

- Static rule-based routing (if/then logic)

- Priority-based routing

- Weighted routing

- Real-time health-based routing

- Performance-driven routing (approval-rate optimization)

Advanced configurations can combine multiple decision layers.

Yes. The back-office provides a configuration interface where business users can:

- Create routing rules

- Define priorities

- Set fallback sequences

- Apply routing per merchant or portfolio

- Configure A/B traffic splitting

No code deployment is required for rule adjustments.

Yes. Built-in resilience includes:

- Automatic retry on soft declines

- Endpoint health monitoring

- Timeout-based failover

- Circuit breaker mechanisms

- Smart fallback to secondary acquirer

This ensures high availability and business continuity.

Yes. Routing can be configured at:

- Portfolio level

- Merchant level

- Merchant group level

- Payment method level

For example, high-risk merchants may have dedicated routing paths.

Typically supported methods include:

- Card payments (3DS and non-3DS)

- Tokenized payments

- Apple Pay / Google Pay

- Installments

- Recurring payments

- Alternative payment methods (APMs)

- Local payment schemes

Each method can have its own routing logic.

Yes. The gateway integrates with:

- EMV 3DS Server

- Directory Server

- ACS connections

Smart Routing can determine whether to:

- Trigger 3DS

- Apply exemption

- Route to specific 3DS provider

- Perform step-up authentication

Yes. It supports:

- Multi-currency processing

- Local acquiring connections

- Cross-border routing

- Dynamic currency conversion (optional)

- FX markup configuration

Smart Routing can prioritize local acquiring to reduce interchange costs.

Yes. Risk tools may include:

- Velocity controls

- BIN and country restrictions

- Blacklists / whitelists

- Fraud scoring integration

- Transaction monitoring

- Chargeback management

Risk decisions can influence routing paths.

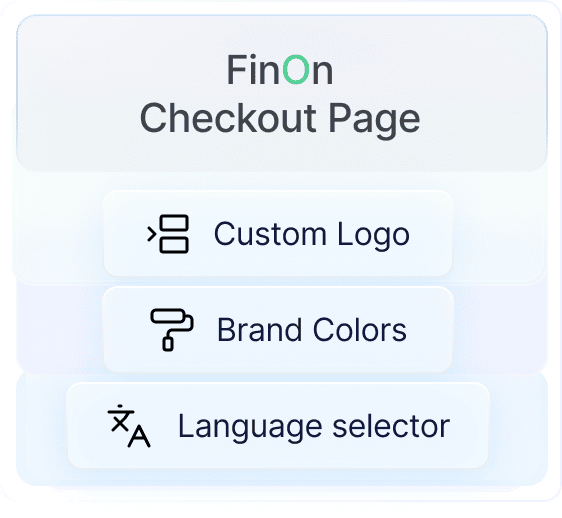

White-label branding includes:

- Custom domain

- Branded payment pages

- Merchant portal branding

- Back-office branding

- API documentation customization

- Custom email templates

The platform appears as a fully owned solution.

Yes. The architecture typically supports:

- Horizontal scaling

- Load balancing

- High TPS processing

- Clustered deployment

- Active-active environments

It is suitable for enterprise-grade payment volumes.

Yes. The gateway provides:

- Unified transaction reporting

- Consolidated settlement reports

- Acquirer comparison analytics

- Approval rate analysis

- Cost analysis per route

- Real-time dashboard monitoring

All data is centralized despite multi-acquirer routing.

Yes. The gateway can operate within:

- Direct acquiring models

- PayFac structures

- Aggregator hierarchies

- Marketplace payment flows

Smart Routing can be applied per sub-merchant.

Launch timelines depend on:

- Number of acquirer integrations

- Required payment methods

- Certification processes

- Branding customization

- Regulatory approvals

However, white-label significantly reduces time-to-market compared to building from scratch.

A White-Label Payment Gateway with Smart Routing enables organizations to:

- Own the customer relationship

- Increase approval rates

- Reduce processing costs

- Avoid vendor lock-in

- Monetize orchestration

- Expand globally with multi-acquirer connectivity

Do you have any other question?

Ready to see the Full Picture?

Let’s connect - and walk you through a personalized demo.

Explore more insights

How to Choose a White Label Payment Gateway Vendor

Selecting the right white-label payment gateway vendor is a key infrastructure decision for PSPs, ac...

Ready to see the Full Picture?

Let’s connect - and walk you through a personalized demo.