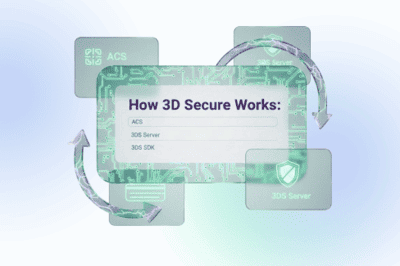

3DS Server

- Optimize authentication flows

- Increase approval rates with frictionless flow

- Get operational transparency & monitoring

is a compliant EMV® 3DS 2.x solution that enables secure and frictionless online payments by connecting merchants, PSPs, and issuers within the 3D Secure flow. It supports on-premise and cloud deployment, integrates with major card schemes, and scales easily across regions and transaction volumes.

Merchant / PSP

3DS Server

Issuer ACSs

Running issuer-grade 3DS requires full control over authentication policies and compliance in complex card portfolios.

Offer 3DS as part of their payment acceptance stack and reduce fraud/chargebacks while protecting conversion

Make 3DS a tool to improve approvals, reduce costs, and ensure reliable routing across multiple PSPs and acquirers

EMV® 3DS 2.x certified and approved by major card schemes, including Visa, Mastercard, AMEX, JCB, and UnionPay.

Supports multiple merchants, acquirers, and PSPs with high availability and seamless scheme integration.

Key Features

Intuitive admin interface with dashboards, logs, and analytics for configuration and transaction monitoring.

Supports SCA and PSD2 requirements. PA-DSS (PCI-SSF) compliant and ready for PCI DSS audits.

Advanced rules engine enables frictionless flows, exemptions, and RBA/TRA to improve approval rates.

Seamless iOS and Android SDKs with fully embedded 3DS authentication inside the merchant app.

Automatically collects device data, communicates with issuers, and triggers challenges only when required.

Use as a standalone SDK or wrap inside PSP or acquirer SDKs for faster merchant onboarding.

Fully compliant with EMV® 3DS specifications and compatible with all major card schemes.

Clear documentation, implementation guides, and dedicated support ensure fast and smooth integration.

Transparent pricing with no hidden fees. Built on open technologies to reduce licensing, support, and operational

Go live in as little as 14 days. Multiple integration options simplify onboarding and deployment.

Designed for high availability and growth. Supports containerization, load balancing, and automatic failover.

Seamless integration with iOS and Android SDKs. Ensures smooth in-app 3D Secure authentication flows.

Go live faster with FinOn's 3DS Server as a Servers - no hosting, no hassle.

Discover moreA 3DS Server is a core EMV® 3-D Secure component used by acquirers, PSPs, and gateways to initiate and manage 3DS authentication flows between:

It handles authentication requests (AReq), responses (ARes), challenge flows (CReq/CRes), and final authentication results.

The 3DS Server is available in two modes:

License (On-Premise):

SaaS (Cloud-Hosted):

Both models support the same EMV 3DS functionality.

The 3DS Server is suitable for:

It supports both domestic and cross-border e-commerce environments.

The server supports:

Including:

Us-on-Us authentication refers to a scenario where:

This reduces latency and improves approval rates.

Yes. The system supports:

This is particularly useful for large banks operating both acquiring and issuing businesses.

Routing decisions can be based on:

If a transaction qualifies as Us-on-Us, it can be routed directly to the internal ACS.

Yes. The 3DS Server can connect to:

Each scheme can have independent configuration and certification, supporting multiple hosts and failover rules.

In License mode:

In SaaS mode:

Certification scope depends on scheme requirements and deployment model.

Yes. The 3DS Server enables:

Risk signals can be enriched via gateway integration.

Yes. The 3DS Server can:

It can function as part of a full payment orchestration ecosystem.

The server supports:

It manages CReq/CRes messaging and session lifecycle.

Yes. The 3DS Server can:

Exemption logic can be integrated with gateway risk engines.

License mode provides:

It is ideal for large banks or regulated entities.

SaaS mode provides:

It is ideal for PSPs and fintechs seeking agility.

Yes. The architecture supports:

It is designed for high TPS environments.

Security features include:

Compliance with scheme security requirements is maintained.

Logical tenant isolation

Multi-tenant PSPs can operate under a single infrastructure.

Yes. Reporting may include:

This helps optimize authentication strategy.

Direct ACS interaction enables:

It is especially valuable for banks operating both issuing and acquiring businesses.

Do you have any other question?

Let’s connect - and walk you through a personalized demo.

Learn how Qi Card, Iraq’s largest digital payments ecosystem, modernized its e-commerce and 3D Secur...

Let’s connect - and walk you through a personalized demo.